Why Gresham’s Law is Important For You

Bitcoin’s legal status as commodity money brings to light Gresham’s Law, an economic principle stating “bad money drives out good.” We explore how to apply Gresham’s Law to the Bitcoin Standard.

Money makes the world go 'round. But what happens when there are different forms of money circulate side by side?

This phenomenon is explained by Gresham’s Law, a centuries-old economic principle stating that "bad money drives out good." As Bitcoin continues its meteoric rise as a digital currency and store of value, the implications of Gresham’s Law are more relevant than ever.

Will Bitcoin be able to take hold as the new medium of exchange of the future?

Or will it be relegated to a nascent store of value as the bad money’s inflationary policy continues incentivizing spending?

While often attributed to British financier Thomas Gresham, ancient Greeks and Romans knew the observation behind Gresham’s Law. They noticed that when coins of varying gold and silver content circulated together, the "bad" coins with lower precious metal content drove the "good" coins out of circulation. People hoard coins with higher gold or silver purity while spending money on "bad" coins of lesser value.

Bitcoin Talk Forum

Historical Origin

In the 1500s, Sir Thomas Gresham articulated the principle that “bad money drives out good” in a letter to Queen Elizabeth I.

The debased currency circulated by King Henry VIII led to a loss of high-quality coins, and silver moved overseas, where it had better value.

Application of Gresham’s Law

This principle explains how inferior currency tends to replace high-quality money in circulation when an artificially imposed exchange rate is enforced.

Digital Currency Context

In the digital age, Gresham’s Law is applicable, with Bitcoin being the new “good money.”

As a nascent store of value, many holders avoid spending Bitcoin during this period due to its appreciation over time, preferring to spend “bad” traditional fiat currencies instead.

Understanding Gresham’s Law

Gresham’s Law refers to the principle that when different forms of currency coexist, the one with lesser intrinsic value (“bad” money) tends to circulate widely. In comparison, the one with greater intrinsic value (“good” money) is hoarded or removed from circulation.

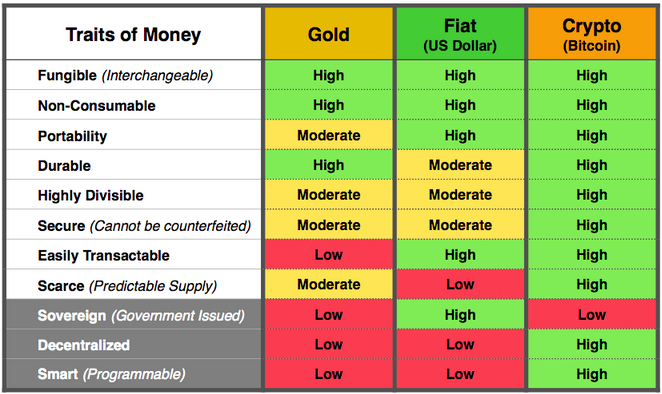

Commodity vs. Fiat Money

Commodity Money: Holds intrinsic value based on the physical worth of precious metals like gold and silver.

Fiat Money: Has no intrinsic value but derives its worth from government backing or decrees.

Key Mechanisms of Gresham’s Law

Hoarding: Individuals perceive commodity currencies to have greater long-term value. Therefore, they stockpile these currencies while using fiat money for daily transactions.

Melting Down: Coins made of valuable metals get melted down and sold for their metallic worth.

Account Settling: Debtors favor settling their accounts with fiat currency because it’s legal tender, even though it has less intrinsic value.

End Result

The cumulative effect is that only inferior money (fiat currency) circulates actively in the economy. As a result, currency devaluation becomes cyclical, potentially contributing to inflation.

For more insights into inflationary and deflationary trends.

New Chapter for Gresham’s Law

Bitcoin introduces a new dimension to Gresham’s Law as a decentralized digital currency. Unlike traditional physical money, Bitcoin is backed by cryptography, features a programmed supply, and gains value from its network effect, setting a distinct path from commodities-based currencies.

Application of Gresham’s Law in the Digital Era

This age-old economic principle raises questions about how it can provide insight into Bitcoin’s impact on monetary systems and its future trajectory.

Inherent Value and Supply

Bitcoin has an inherent value and a limited supply, which is in stark contrast to the theoretically unlimited supply of fiat currencies.

Coexistence with Fiat Currencies

For over a decade, Bitcoin and fiat currencies have coexisted, serving as payment methods. This demonstrates the practical applications and acceptance of Bitcoin alongside traditional money.

Key Differences from Traditional Applications of Gresham’s Law

Lack of Physical Form

Unlike physical money, Bitcoin cannot be “driven out” of circulation since it exists purely as a digital asset on the blockchain.

Utility and Value

Bitcoin serves multiple functions—it operates as a payment network, an uncorrelated asset, and a monetary system beyond government control. This multifaceted utility significantly influences its value and distinguishes it from traditional monetary frameworks.

Human Psychology and Gresham’s Law

When considering Bitcoin through the lens of Gresham’s Law, human psychological elements remain significant. People use Bitcoin as a savings vehicle, similar to precious metals, due to its limited supply and potential for appreciation, driving its use over fiat currencies when both are options for saving (learn more about saving with Bitcoin).

Utility and Spending Incentives

Beyond merely serving as a store of value, Bitcoin provides a unique utility that shifts incentives from hoarding. Its acceptance as a mainstream form of payment could encourage the spending of fiat currencies while retaining Bitcoin for savings, leveraging its first-mover advantage and growing network effect.

Impact on Traditional Financial Systems

The relationship between Bitcoin, fiat currencies, and Gresham’s Law presents a complex interplay of money, technology, and economic theory. This interaction could potentially reshape traditional banking and monetary policies in significant ways, presenting two primary routes:

Influence on Banking

Bitcoin poses a distinct challenge to traditional banking systems by offering an alternative that operates outside of government control and conventional banking mechanisms (explore the impact on banking).

Shifts in Monetary Policy

As Bitcoin continues to gain acceptance and influence, it may prompt shifts in how monetary policies are formulated and implemented, challenging existing financial frameworks and necessitating new approaches to economic management.

Route 1: Bitcoin Accepted as a Means of Payment

Picture this: a country where Bitcoin is embraced as a legitimate form of payment alongside traditional fiat currencies. Gresham’s Law could come into play in this scenario but with a twist. Instead of "bad" money drives out "good" money, we might witness a shift where Bitcoin becomes the preferred form of payment, thanks to its advantages over fiat currencies:

Currency competition and innovation: The acceptance of Bitcoin as a means of payment could create healthy competition between Bitcoin and fiat currencies. Governments and traditional banking systems may need to adapt to this new reality by introducing innovative financial products and services to stay relevant and attract users.

Enhanced financial inclusivity: Bitcoin’s decentralized nature can provide financial access to those underserved by traditional banking systems. It could empower individuals in areas with limited banking infrastructure, allowing them to participate in the global economy.

Altered monetary policies: With Bitcoin entering the mix, governments may need to reassess their monetary policies. The fixed supply of 21 million bitcoins could challenge central banks' ability to control money supply and ensure price stability.

Vendor incentives: Since Bitcoin does not rely on layers of intermediaries to process transactions and move value, businesses are incentivized to adopt the technology as a cost-savings mechanism. As more businesses begin to accept Bitcoin, the public may very well follow suit, especially if those businesses pass their cost savings on to their customers as well.

Route 2: Hostility and Capital Flight

Now, let’s take a turn down a different path—one where governments continue their hostility towards Bitcoin, leading to the outflow of Bitcoin-denominated wealth from the country, as alluded to in the book "Sovereign Individual“:

Government crackdowns and restrictions: In this scenario, governments perceive Bitcoin as a threat to threatening their control over monetary systems and attempt to suppress it through strict regulations or bans. This hostility might only drive the use of Bitcoin underground and limit its potential benefits.

Capital flight and currency devaluation: Faced with government resistance, individuals may opt to move their wealth out of the country by converting it into Bitcoin, a portable bearer asset that can easily cross borders. This capital flight could pressure fiat currencies, leading to currency devaluation and economic instability.

Impact on traditional banking: As individuals embrace Bitcoin to protect their wealth, traditional banking systems in hostile countries could experience a decline in deposits and face challenges in managing capital flows. Banks may need to adapt their services to cater to the changing financial landscape or risk becoming obsolete.

Remember, these two routes present contrasting possibilities and would have varied implications for traditional banking and monetary policies. The acceptance or hostility towards Bitcoin depends on how governments and financial institutions perceive and adapt to this technological disruption.

My Bigger Tricks

The Potential for Bitcoin as "Good" or "Bad" Money: A Gresham’s Law Perspective

In the wild world of money, where Bitcoin roams alongside traditional fiat currencies, how does it fare in the eyes of Gresham’s Law?

Could it be considered "good" or "bad" money?

Let’s dive in and find out!

Bitcoin as "Good" Money

When we say Bitcoin could be seen as "good" money, we mean it’s the preferred choice for transactions and store of value. Here’s why Bitcoin might earn that shiny "good" money title:

Transcending boundaries: Bitcoin operates globally and is accessible to anyone with an internet connection. It’s not tied to any particular country or central authority. This borderless nature allows for seamless and secure cross-border transactions, making it a convenient option.

Security and privacy: Bitcoin offers a high level of security, as cryptographic technology protects transactions. It also allows for anonymous transactions, giving individuals control over their financial information.

Limited supply: Unlike fiat currencies that can be printed to no end, there will only ever be 21 million Bitcoin. This scarcity, combined with growing demand, could lead to price appreciation. It’s like owning a limited edition, except instead of Beanie Babies, it’s digital gold!

Bitcoin as "Bad" Money

On the flip side, Bitcoin might get labeled as "bad" money if it falls short in certain areas. Here are a few aspects that could contribute to this less flattering designation:

Volatility: Bitcoin’s price can resemble a roller coaster ride on a bumpy road. The value can fluctuate wildly, which might deter some from using it as a stable medium of exchange, at least during the monetization phase of adoption.

Limited acceptance: While increasing in popularity, Bitcoin has yet to achieve widespread adoption as a payment method. You can’t exactly pay for your morning coffee or groceries with it everywhere you go, unless you stumble upon a Bitcoin-savvy vendor or cafe. If businesses remain intransigent in their acceptance, then it might be difficult to gain traction as an everyday-use currency.

Learning curve: Bitcoin is a different beast from traditional money. It requires a degree of technical understanding to set up wallets, manage private keys, and navigate the ecosystem. This learning curve could act as a barrier to widespread adoption.

The Interplay Continues

Many argue that Bitcoin is still in its earliest stages of adoption.

As Bitcoin grows and matures, the volatility is expected to decline, making Bitcoin more suitable for everyday transactions. That being said, despite the current volatility, many are choosing to live on a Bitcoin standard regardless.

This trend could continue to accelerate with fiat monetary debasement over time.

Addressing the Limitations of Applying Gresham’s Law to the Bitcoin Market

Ah, Gresham’s Law. It’s a nifty economic principle that helps us understand how "bad" money can squeeze out "good" money. However, when it comes to applying Gresham’s Law to the Bitcoin market, we need to consider its limitations and potential criticisms.

Technological Differences

Bitcoin is a whole different beast compared to traditional fiat currencies. Its underlying technology and features can challenge the application of Gresham’s Law in a couple of ways:

Digital vs. physical: Bitcoin exists purely in the digital realm, unlike physical coins or paper bills. This digital nature can affect people’s perception of its value and utility, making it harder to compare directly to physical currencies.

Uniqueness and scarcity: Bitcoin’s limited supply and uniqueness set it apart from fiat currencies. Unlike traditional money, Bitcoin cannot be easily replicated or printed at will. This scarcity factor introduces a whole new dynamic that may not neatly fit into Gresham’s Law’s framework.

Adoption Challenges

Limited acceptance: Bitcoin’s acceptance as a means of payment is still in its early stages. While some businesses and individuals embrace it, it’s not yet universally accepted. This limited adoption could hinder the smooth operation of Gresham’s Law, as the battle between "good" and "bad" money requires widespread usage.

Volatility and Store of Value Concerns

Bitcoin’s notorious price volatility can make it a less desirable store of value or medium of exchange for the risk-averse. Others may be hesitant to spend their Bitcoin if they expect its value to skyrocket in the future, leading to higher savings rates and less circulation.

Utility Differences

Transaction speed and scalability: Bitcoin’s underlying blockchain technology comes with speed and scalability limitations.

The time it takes to process transactions and the number of transactions the network can handle per second can impact its practicality as a medium of exchange.Though second-layer protocols alleviate these concerns, some argue that later adopters may be relegated to second-class citizen status with Bitcoin service providers rather than fully owning the Bitcoin themselves.

Privacy and Anonymity

Bitcoin offers a degree of privacy but is not entirely anonymous. Transactions can be traced on the public blockchain, which might deter some individuals from fully embracing it for everyday transactions.

Bitcoin as "Good" money: Bitcoin has the potential to be preferred for transactions and as a store of value due to its borderless nature, security features, and limited supply. It’s like a globetrotting superhero with cryptographic armor and a limited-edition cape. Pretty impressive, right?

Bitcoin as "Bad" money: On the flip side, Bitcoin faces challenges that might hinder its acceptance as a stable medium of exchange. Volatility, limited adoption, and a steep learning curve can make it a little less dazzling in the eyes of Gresham’s Law. But fear not, for these challenges may fade away with time and adoption like a bad hair day.

Technological, adoption, and utility differences: Bitcoin’s digital nature, unique scarcity, limited acceptance, scalability concerns, and privacy features introduce complexities that may not neatly align with Gresham’s Law. It’s like trying to fit a square peg into a round hole, but the pieces might just come together with some wiggling and adjustment.

Join Swan Bitcoin today. Happy Bitcoin-ing!

Swan is a leading Bitcoin financial services company with more than 120,000 clients and 170 employees, operating globally. Established in 2019, Swan helps individuals and institutions to understand and invest in Bitcoin. The Swan app simplifies Bitcoin purchases with instant and recurring buys. Swan IRA provides a tax-advantaged solution for saving Bitcoin in retirement accounts.

For HNWIs and businesses, Swan Private provides white-glove service for large purchases, treasury solutions, and employee Bitcoin benefits. With Swan Vault, clients can easily custody their own Bitcoin with peace of mind. Financial advisors trust Swan Advisor for client Bitcoin allocations, backed by world-class custody and educational content.

Swan Managed Mining provides clients with fully segregated and dedicated mining operations, catering to their unique requirements, opportunities, and strategic advantages. Swan prides itself on exceptional client service, making Bitcoin accessible to all. For more information, please visit swan.com.

Swan IRA — Real Bitcoin, No Taxes*

Hold your IRA with the most trusted name in Bitcoin.

Mickey Koss became a freelance writer in the Bitcoin space in an attempt to build a proof of work portfolio for when he left the Army. He graduated from West Point with a degree in Economics before serving in the Army for nearly a decade. He became orange pilled in graduate school and is now a regular contributor to Forbes, Bitcoin Magazine, and Bitcoin News. He’s been on popular podcasts such as BTC Sessions’ Why Are We Bullish, and is a regular on Café Bitcoin.

More from Swan Signal Blog

Thoughts on Bitcoin from the Swan team and friends.

Best Bitcoin ETF Fees: Lowest to Highest (May 2024)

In this guide, we analyze and present the top 10 Bitcoin ETFs with the lowest fees for cost-effective investing.

What Is BTC Hashrate? Why You Should Care (May 2024 Update)

Bitcoin hashrate? Sounds confusing, but its not. Learn the role Bitcoin’s hashrate plays and why its important.

Swan Announces Managed Bitcoin Mining Service

Swan Bitcoin launches Managed Mining service for institutional investors, announces strategic collaboration with Tether, targets 100 EH by 2026.